Hospitality Sector Index

- katherinedoggrell

- Apr 17

- 3 min read

The Moore Kingston Smith monthly hospitality sector report provides you with a valuable and timely indication of the month-on-month and year-on-year changes occurring within the sector.

Overall sector performance

Hospitality sector treads water as February’s event led boost fades.

Improved weather shift supports pubs seasonal growth, but wider growth remains elusive.

Casual dining squeezed as households continue to pull back on discretionary spend.

Labour costs remain the main margin lever, as revenue growth stays out of reach.

Value perception remains critical as households stay cost-conscious.

Restaurants, pubs and bars - March 2026

Fine dining

March followed a familiar seasonal slowdown for fine dining, with demand easing after the February trading period. Revenue fell 3.8% month on month, while labour hours declined by 2.1%, reflecting the limited flexibility operators have when maintaining service standards. The seasonal downturn was more pronounced than last year, when March revenue dipped by just 0.6%, pointing to a sharper pullback in discretionary spend in the current environment.

Despite this, year‑on‑year performance was resilient. Revenue grew 2.9% versus March 2025, while labour hours were 4.3% lower. This reflects the relative strength of high‑end, occasion‑led demand, allowing revenues to hold up without expanding operational scale. At the same time, tighter staffing control points to improved resource management across the segment.

Casual dining

Casual dining delivered a steady month on month result, with revenue rising 0.7% as labour hours fell slightly. This compares favourably with the same seasonal period last year, when March delivered only marginal revenue growth and rising labour input – suggesting improved short‑term operational discipline in the current cycle.

To remove the effect of seasonality it is essential to understand the year‑on‑year trends which show that like-for-like revenue fell sharply by 9.3% versus March 2025, a decline that is materially worse than other categories in the hospitality sector. This reflects the ongoing impact of the cost-of-living crisis, with discretionary, mid-market dining proving the most exposed as households prioritise essential spending. Labour hours were reduced broadly in line with sales, indicating swift reaction by operators, but also underlining how exposed casual dining has become during traditionally stable spring trading months.

Pubs & bars

March delivered a clear seasonal uplift for pubs and bars, with revenue up 8.1% on February 2026, supported by longer evenings and improving weather. Operators increased labour hours by 5.4%, leaning into demand rather than chasing efficiency alone. The seasonal revenue uplift was stronger than last year, when March revenue growth was closer to mid‑single digits but with tighter labour deployment.

Year on year, revenue rose 7.6%, reinforcing the segment’s resilience during a period that typically marks the early stages of the spring trading cycle. Unlike other segments, pubs and bars appear to have enjoyed a comparatively strong start to 2026, delivering inflation beating revenue growth.

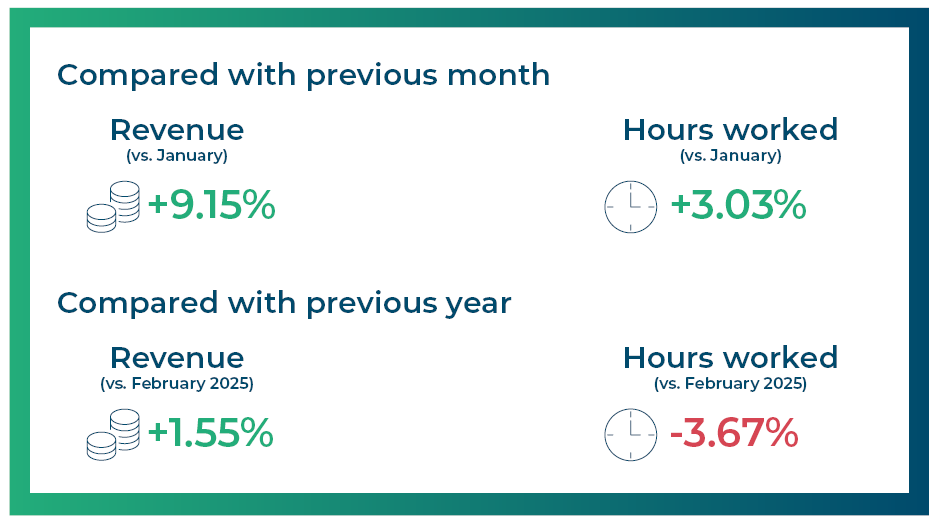

Hotels - February 2026*

*The hotel data reflects a period one month earlier than the restaurant data due to an industry reporting lag.

Hotel performance in February 2026 remained consistent with seasonal expectations, building on the typical early‑year recovery in business travel and conference activity post the January lull. Compared with last year – similar revenue growth required a much greater expansion in labour. The current performance points to improved operational efficiency and tighter workforce management.

On a year‑on‑year basis, revenue increased 1.6% while labour hours fell 3.7%, representing a more efficient performance than March 2025, when similar revenue growth required higher staffing levels. This suggests operators are managing labour costs more tightly, balancing modest demand growth with disciplined cost control to protect margins.

Comments