Hospitality Sector Index

- katherinedoggrell

- Jun 18

- 3 min read

The Moore Kingston Smith monthly hospitality sector report provides you with a valuable and timely indication of the month-on-month and year-on-year changes occurring within the sector.

Restaurants, pubs and bars –May 2026

May hospitality update: shoots of recovery emerge across sectors, with fine dining leading the way.

Hospitality at a glance

Monthly growth returned across all sub-sectors, signalling seasonal momentum.

Fine dining led the charge, driven by strong Central London demand.

Casual dining edged forward, though demand remains highly price-sensitive.

Pubs and bars held steady, with West London standing out.

Hotels edged forward, but recovery is still uneven.

Sub-sector performance

Fine dining

Fine dining delivered a strong performance in May, with revenue rising 8.34% month on month and labour hours increasing by 1.30%. Growth was particularly pronounced in Central London, where revenues increased by 15.13%, highlighting a more concentrated rebound in key urban markets.

Growth was driven by increased demand for occasion‑led experiences, with consumers showing a willingness to spend at the top end of the market. Operators responded by selectively increasing staffing levels while maintaining disciplined cost control.

Year on year, the sub-sector showed clear resilience, revenue up 8.96% compared to May 2025, and strong cost control, as labour hours fell by 1.40% in the same period.

This demonstrates the strength of premium demand despite the cost-of-living crisis. This sub-sector of the hospitality sector has also sustained a focus on productivity, as operators prioritise margin efficiency and leaner operating models to protect profitability.

Casual dining

Casual dining remains under pressure, with operators continuing to navigate cost-sensitive consumer behaviour and reduced dining frequency.

May provided some relief, supported by seasonal trading and improved footfall, with revenue increasing by 3.92% and labour hours rising by 0.51% month on month.

However, the improvement remains measured rather than decisive, with operators still reliant on value-driven demand and no clear sign of sustained acceleration in underlying activity.

Against this backdrop, year-on-year performance continues to highlight the challenge facing the sector, with revenue down 5.74% and labour hours reduced by 7.66% compared with May 2025.

Mid-market operators will therefore need to keep adapting their offer to remain competitive as trading conditions remain fragile.

Pubs & bars

Pubs and bars remain a resilient driver of sector performance, with steady seasonal demand, disciplined labour management and notable strength in West London (revenue up 18.13% on prior year supporting continued growth).

On an annual basis, pubs and bars remain the strongest performing sub-sector, with revenue up 6.49% versus May 2025, while labour hours declined slightly by 1.02%.

The sub-sector also maintained positive seasonal momentum in May, with revenue rising 0.82% month on month and labour hours increasing by 0.99%. Performance points to steady underlying demand, with limited volatility and operators aligning staffing closely to incremental changes in trade.

This ongoing outperformance highlights the sector’s ability to balance value appeal with efficient labour management, reinforcing its position as a key driver of hospitality resilience. Operators will now be looking ahead to the expected uplift in demand from the FIFA World Cup, which begins in June, as a potential boost to footfall and sales.

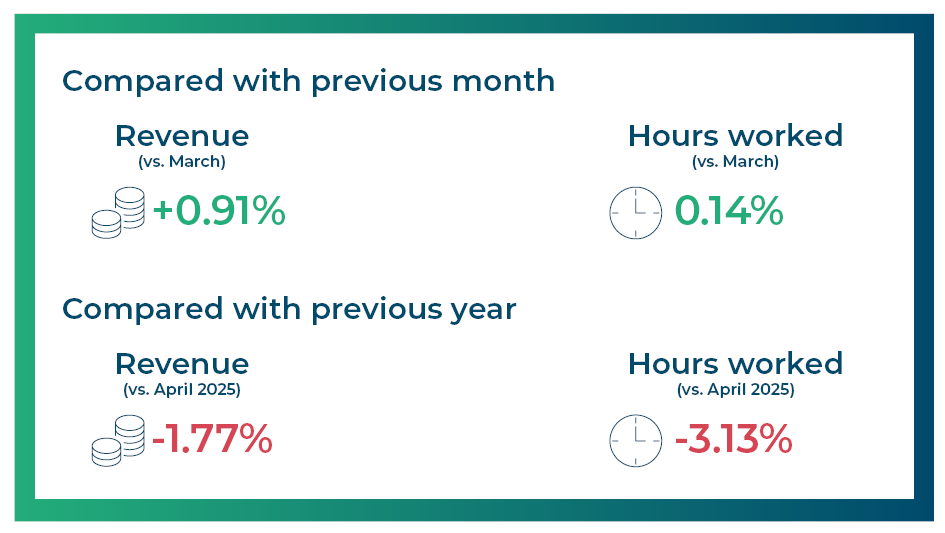

Hotels – April 2026*

*The hotel data reflects a period one month earlier than the restaurant data due to an industry reporting lag.

Hotels continued to make steady but limited monthly progress, with revenue increasing by 0.91% and labour hours rising by 0.14%, suggesting that operators are seeing slight improvement in demand but are still cautious in how they resource the business.

Rather than indicating a broad-based recovery, the limited movement points to a measured improvement in occupancy and trading conditions, with staffing levels being adjusted carefully to preserve margins.

The year-on-year picture remains more challenging, with revenue down 1.77% and labour hours reduced by 3.13% compared with April 2025, underlining the uneven nature of the recovery.

The sub-sector continues to navigate uneven demand, with cost control and operational efficiency remaining a priority as recovery progresses at a measured pace.

Comments